Bl View MCP

Portfolio Optimization MCP based on black-litterman model

Installation

npx bl-view-mcpAsk AI about Bl View MCP

Powered by Claude · Grounded in docs

I know everything about Bl View MCP. Ask me about installation, configuration, usage, or troubleshooting.

0/500

Reviews

Documentation

Black-Litterman Portfolio Optimization MCP Server

![]()

Black-Litterman portfolio optimization MCP server for AI agents

Works with Claude Desktop, Windsurf IDE, Google ADK, and any MCP-compatible AI

Features

- Portfolio Optimization - Black-Litterman model with sensitivity analysis

- Investor Views - Absolute/relative views with confidence levels

- Backtesting - Strategy comparison, drawdown analysis, timeseries

- Asset Analysis - Correlation matrix, VaR, per-asset statistics

- Dashboard Generation - Visualization hints for AI-generated charts

- Multiple Assets - S&P 500, NASDAQ 100, ETF, Crypto, custom data

Quick Start

Option 1: Smithery (Easiest - No Installation!) 🌟

Install via Smithery in one command:

npx @smithery/cli install @irresi/bl-view-mcp --client claude

Or visit smithery.ai/server/@irresi/bl-view-mcp and click:

- "Add to Claude Desktop" - One-click setup

- "Add to ChatGPT" - Direct integration

- "Run" - Test in browser instantly

No Python/uv installation needed! Smithery hosts the server for you.

Option 2: Local Installation (uvx)

For offline use or development:

Step 1: Find uvx path

Run in terminal:

which uvx

# Example output: /Users/USERNAME/.local/bin/uvx

If uvx is not installed:

curl -LsSf https://astral.sh/uv/install.sh | sh

Step 2: Configure Claude Desktop

Config file location:

- macOS:

~/Library/Application Support/Claude/claude_desktop_config.json - Windows:

%APPDATA%\Claude\claude_desktop_config.json

File content (replace with your uvx path):

{

"mcpServers": {

"black-litterman": {

"command": "/Users/USERNAME/.local/bin/uvx",

"args": ["black-litterman-mcp"]

}

}

}

Step 3: Restart Claude Desktop

Cmd+Q (macOS) or fully quit and restart

Usage

Ask Claude:

"Optimize a portfolio with AAPL, MSFT, GOOGL. I think AAPL will return 10%."

First run: S&P 500 data auto-downloads (~30 seconds)

Tip: Want charts or dashboards? Just ask: "Show me a dashboard with the results" or "Create a visualization of the portfolio weights"

Example Use Cases

Try these prompts with Claude:

Note: Default period is 1 year for all tools. All returns are annualized - when you say "outperform by 40%", it means 40% annual return expectation.

Basic Optimization + Visualization

Optimize a portfolio with AAPL, MSFT, GOOGL, NVDA. I am confident that NVDA will outperform others by 40%. Show me a dashboard.

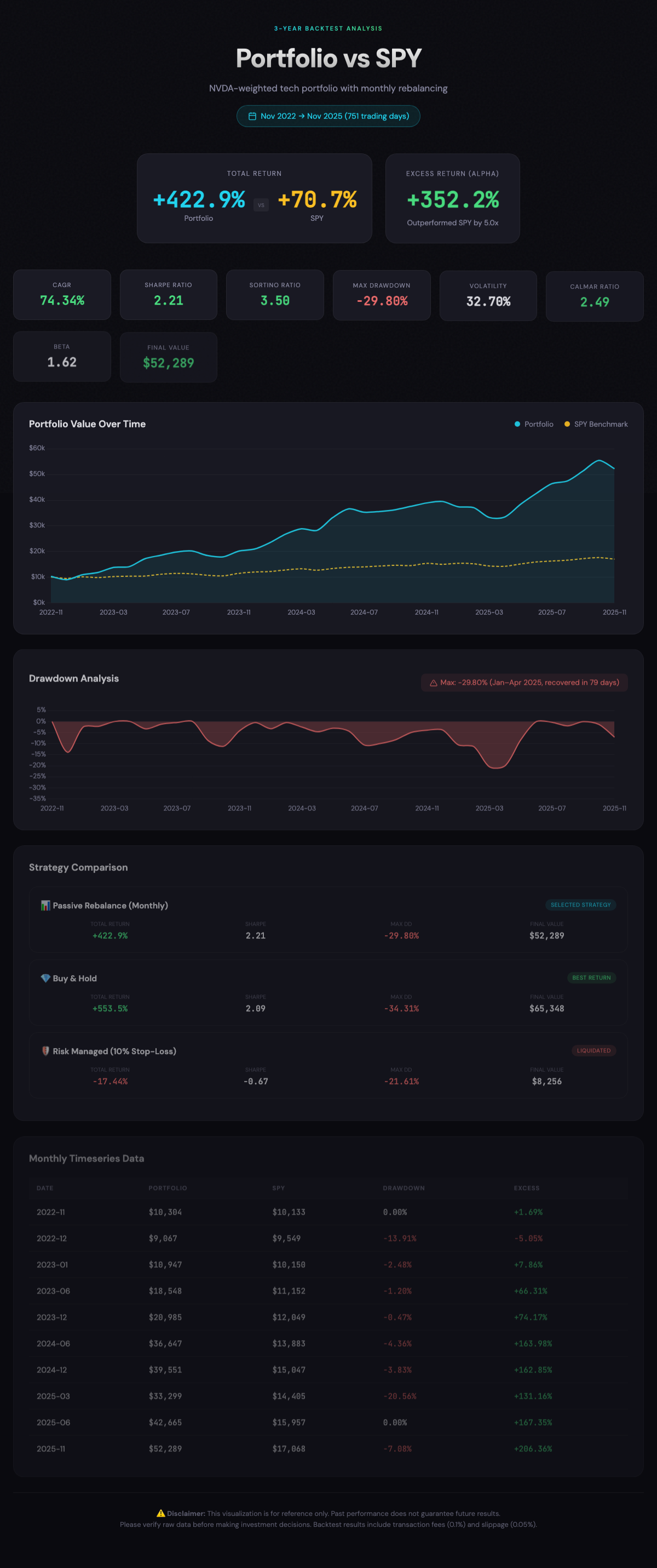

Backtesting with Benchmark

Backtest the above optimized portfolio for 3 years and compare with SPY.

Strategy Comparison

Compare buy_and_hold, passive_rebalance, and risk_managed strategies for this portfolio.

Correlation Analysis

Analyze the correlation between NVDA, AMD, and INTC.

Sensitivity Analysis

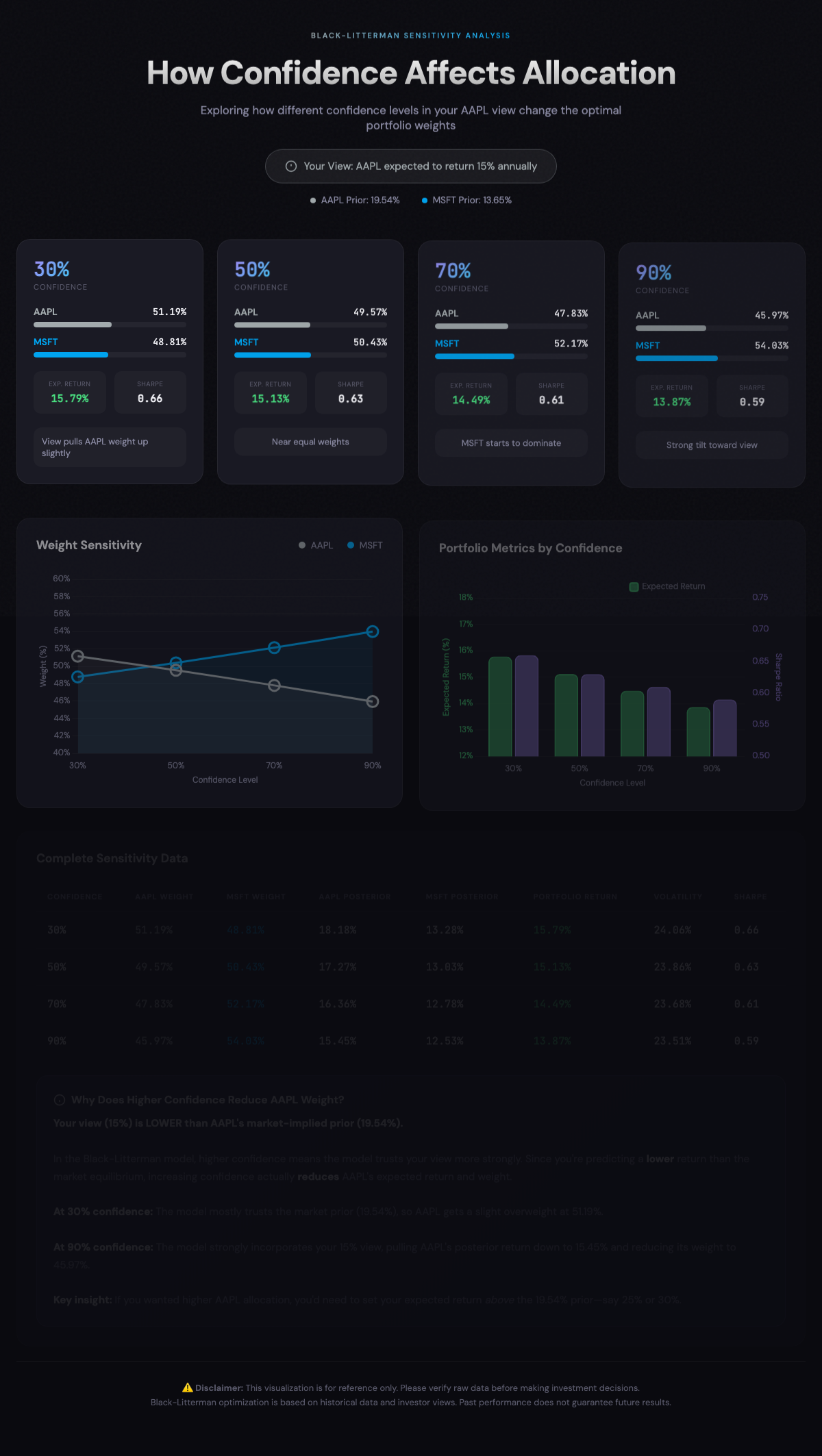

Create a portfolio with AAPL and MSFT. I expect AAPL to return 15%. Run sensitivity analysis with confidence levels 0.3, 0.5, 0.7, 0.9.

Demo Dashboards

Generated using the example prompts above with Claude Desktop:

Click images to view interactive HTML dashboards:

| Optimization | Backtest | Strategy |

|---|---|---|

|  |  |

| Correlation | Sensitivity |

|---|---|

|  |

Other Installation Methods

pip (Python Package)

Install directly from PyPI:

pip install black-litterman-mcp

Then configure your MCP client to run:

black-litterman-mcp # or bl-view-mcp, bl-mcp

Requires Python 3.11+. Data auto-downloads on first use.

Windsurf IDE

.windsurf/mcp_config.json:

{

"mcpServers": {

"black-litterman": {

"command": "/Users/USERNAME/.local/bin/uvx",

"args": ["black-litterman-mcp"]

}

}

}

From Source (Developers)

git clone https://github.com/irresi/bl-view-mcp.git

cd bl-view-mcp

make install

make download-data # S&P 500 data

make test-simple

Docker

docker build -t bl-mcp .

docker run -p 5000:5000 -v $(pwd)/data:/app/data bl-mcp

Google ADK Web UI

Test with Google ADK (Agent Development Kit):

# Terminal 1: Start MCP HTTP server

make server-http # localhost:5000

# Terminal 2: Start ADK Web UI

make web-ui # localhost:8000

Open http://localhost:8000 in browser

Requires

make install(includes google-adk dependency)

Supported Datasets

| Dataset | Tickers | Description |

|---|---|---|

snp500 | ~500 | S&P 500 constituents (default) |

nasdaq100 | ~100 | NASDAQ 100 constituents |

etf | ~130 | Popular ETFs |

crypto | ~100 | Cryptocurrencies |

custom | - | User-uploaded data |

PyPI install: S&P 500 data auto-downloads on first run

Source install: Download additional datasets manually

make download-data # S&P 500 (default)

make download-nasdaq100 # NASDAQ 100

make download-etf # ETF

make download-crypto # Crypto

MCP Tools

optimize_portfolio_bl

Calculate optimal portfolio weights using Black-Litterman model.

optimize_portfolio_bl(

tickers=["AAPL", "MSFT", "GOOGL"],

period="1Y",

views={"P": [{"AAPL": 1}], "Q": [0.10]}, # AAPL expected 10% return

confidence=0.7,

investment_style="balanced" # aggressive / balanced / conservative

)

Views examples:

# Absolute view: "AAPL will return 10%"

views = {"P": [{"AAPL": 1}], "Q": [0.10]}

# Relative view: "NVDA will outperform AAPL by 20%"

views = {"P": [{"NVDA": 1, "AAPL": -1}], "Q": [0.20]}

VaR Warning: When predicted returns exceed 40%, EGARCH-based VaR analysis is automatically included in the warnings field.

backtest_portfolio

Validate portfolio strategy with historical data.

backtest_portfolio(

tickers=["AAPL", "MSFT", "GOOGL"],

weights={"AAPL": 0.4, "MSFT": 0.35, "GOOGL": 0.25},

period="3Y",

strategy="passive_rebalance", # buy_and_hold / passive_rebalance / risk_managed

benchmark="SPY"

)

get_asset_stats

Get asset statistics including VaR, correlation matrix, and covariance matrix.

get_asset_stats(

tickers=["AAPL", "MSFT", "GOOGL"],

period="1Y",

include_var=True # Set False for faster response (skips EGARCH VaR)

)

# Returns: assets (price, return, volatility, sharpe, var_95, percentile_95),

# correlation_matrix, covariance_matrix

upload_price_data

Upload external data (international stocks, custom assets, etc.).

# Direct upload (small data)

upload_price_data(

ticker="005930.KS", # Samsung Electronics

prices=[

{"date": "2024-01-02", "close": 78000.0},

{"date": "2024-01-03", "close": 78500.0},

...

],

source="custom"

)

# Or load from file (large data)

upload_price_data(

ticker="CUSTOM_INDEX",

file_path="/path/to/data.csv",

date_column="Date",

close_column="Close"

)

list_available_tickers

Query available tickers.

list_available_tickers(search="AAPL") # Search

list_available_tickers(dataset="snp500") # S&P 500 only

list_available_tickers(dataset="custom") # Custom data

Documentation

| Document | Description |

|---|---|

| docs/TESTING.md | Testing guide |

| docs/ARCHITECTURE.md | Technical architecture |

Tech Stack

- MCP Server: FastMCP

- Optimization: PyPortfolioOpt

- Risk Model: arch (EGARCH)

- Data: yfinance, ccxt (crypto)

License

MIT License - LICENSE

Troubleshooting

"spawn uvx ENOENT" / "uv binary not found"

Claude Desktop may not recognize system PATH. Use absolute path:

which uvx

# Use the output path in config

"Data file not found"

Source install:

make download-data

PyPI install: Auto-downloads on first run (~30 seconds).

"uv: command not found"

curl -LsSf https://astral.sh/uv/install.sh | sh